SPECIAL PROVISION RELATED TO INVESTMENT INCOME.

When NRIs invest in certain Indian assets, they are taxed at 20% on the income earned. If only special investment income has during the financial year and TDS has been deducted, then such an NRI is not required to file an ITR.

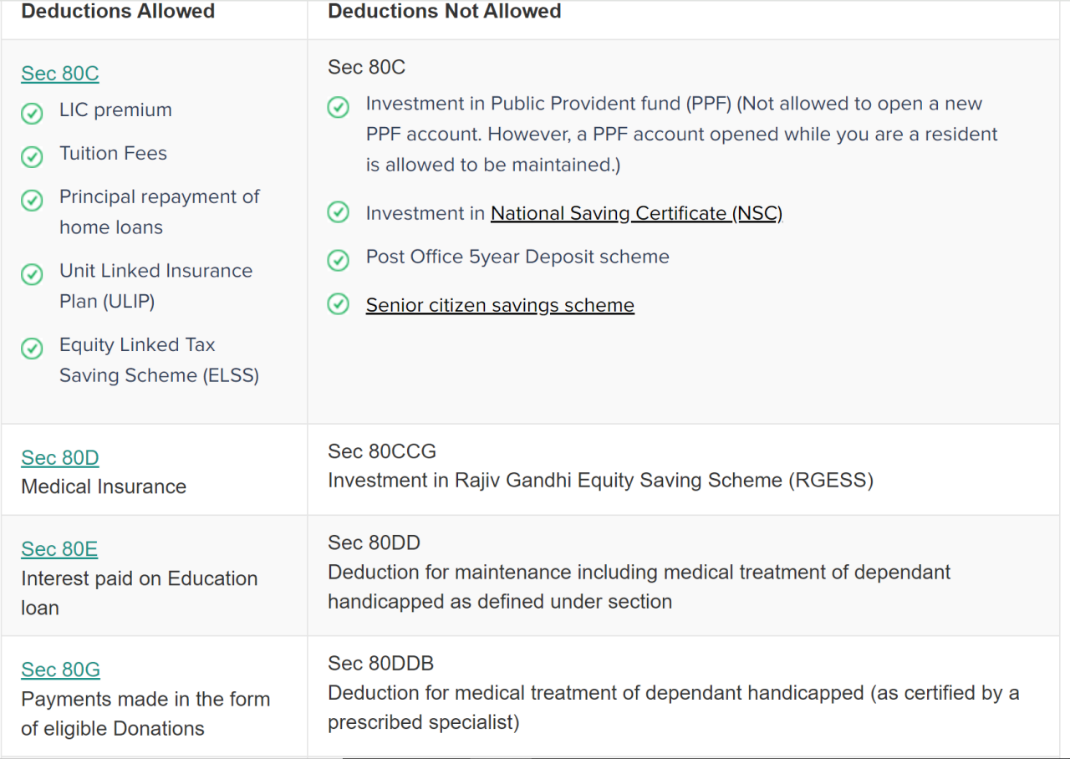

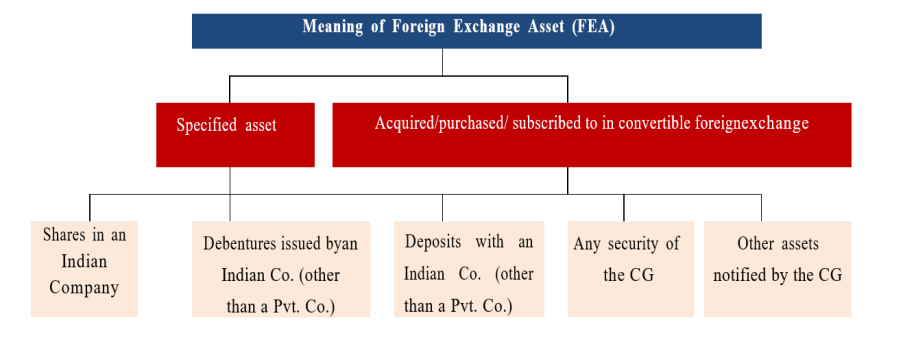

Investments that qualify for special treatment.

Income derived from the following Indian assets acquired in foreign currency:

Note: No deduction under Section 80 is allowed while calculating investment income.

— –

Continue Read:

NRI Taxation Simplified:Understanding Residential Status and Taxes-Part 1

Understanding NRI Accounts and Taxation: Types and Implications — Part 2

Navigating NRI Capital Gains and Taxation: A Comprehensive Guide for Post-2018 Rules — Part — 3

Repatriating Property Sale Proceeds for NRIs: Process and Tax Implications — Part -4

Taxation Insights for Non-Resident Artistes, Entertainers, and Sportspersons in India — Part 5

Disclaimer:

This Article/Blog has been contributed by Butchibabu Gorantla, B.Com, FCA, FCS, Chartered Accountant. This article/blog is posted with due authorization from the author for the academic purposes. The views and opinions expressed herein are those of the author and don’t constitute a legal advice to any user.

Related Posts

A Comprehensive Overview of the Finance Bill 2024

The Finance Bill 2024, introduced in the Lok Sabha, seeks to implement the financial proposals…

The Provisions of the Finance Bill, 2024: A Comprehensive Overview

The Finance Bill, 2024, introduces several amendments to the Income-tax Act, 1961, and other related…

Understanding the Income Tax Slab Rates for FY 2023-24, AY 2024-25: New vs. Old Tax Regimes

The income tax slab rate is the percentage of tax you pay on your income,…

Which ITR Form is Right for You? Find Out Now!

Filing your Income Tax Return (ITR) in India is an essential responsibility. However, with various…