Types of NRI Accounts ?

There are various types of NRI Accounts that are available to an NRI Investor. Some of the major ones are-

Non-Resident Ordinary (NRO) Savings Account/ Fixed Deposit Account

NRE Accounts are maintained in INR. This means that when you deposit the money in the NRE Account, the foreign currency is converted to Indian rupees at the prevailing foreign exchange rates.

It is mainly used to house your savings from income that you have earned abroad.

The principal amount, as well as the interest, are fully repatriable, i.e., transferable.

The interest income earned on the amount in an NRE account is non-taxable in India.

You can have other NRIs or Resident Indian (who is a close relative as per Companies Act 2013) as joint account holders in NRE Accounts. In case Resident Indian is added as Joint holder the mode of operation will be ‘Former or Survivor’.

- Non-Resident External (NRE) Savings Account/ Fixed Deposit Account

- NRO Accounts are maintained in INR. This means that when you deposit the money in the NRO Account, the foreign currency is converted to Indian rupees at the prevailing foreign exchange rates.

- It is used to house funds from your income that you have earned from India or abroad.

- Income like rent, dividend, pension, etc. can be sent abroad through the NRO Account.

- Interest income earned on the amount in an NRO Account is liable for TDS or Tax Deductible at Source.

- You can have other NRIs or Resident Indian as joint account holders in NRO Accounts. In case Resident Indian is added as Joint holder the mode of operation will be ‘Former or Survivor’,

Foreign Currency Non -Resident (FCNR) Fixed Deposit Account

- Foreign Currency Non -Resident Accounts have to be opened and maintained in foreign currency.

- Your principal amount and the interest in an FCNR Account are fully repatriable, i.e., transferable

- Interest income earned on your money in an FCNR account is non-taxable in India.

- You can also opt for other products like NRE/NRO Current account, NRE Recurring Deposit RFC Savings/ RFC Deposits etc.

PART 2B

TYPES OF IncomeS of NRI & its taxability

- The common types of income earned by NRIs in India & its taxability:

Income from other sources:

- Interest on NRO accounts: The interest is taxable in India as per the provisions of Section 195 of the tax Act.

- Interest on NRE accounts: The interest earned on such accounts is exempt in India as long as the status of the account holder is NRI as

- per FEMA regulation and not Income Tax Act.

- Interest on FCNR deposit: The interest earned is exempt from tax in India in the hands of NRI. The NRI status must be as per Income Tax Act and not FEMA. Further, the same is also exempt in the hands of returning Indian having RNOR status.

- Maturity proceeds of PPF and interest on PPF account: Not taxable

- Maturity proceeds of Insurance policies: The taxability or exemption of the proceeds depends upon the conditions of Section 10(10D) of the Income Tax Act. As per the section:

- For policies issued before 01.04.2012 — if the premium paid on the policy does not exceed 20% of the sum assured — Maturity proceeds including bonus is exempted.

- For policies issued after 01.04.2012 — if the premium paid on the policy does not exceed 10% of the sum assured — Maturity proceeds including bonus is exempted.

- Pension income: Pension earned and received in India is taxable in India.

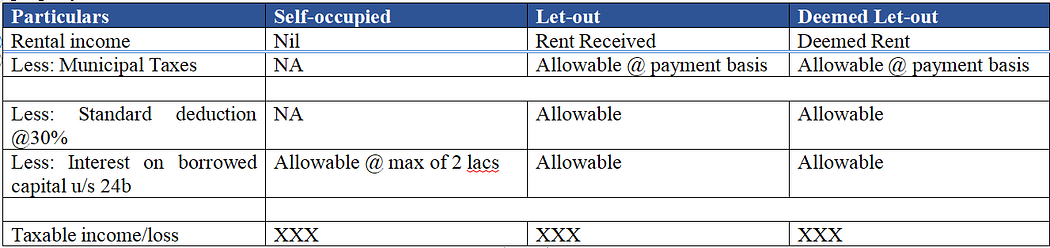

Rental Income: (IFHP)

- The rental income is taxed under the head — “Income from house property”.

- NRIs can hold any number of properties in India. The income from property are taxed under three categories as under:

-Self-occupied property

-Let-out property

-Deemed to be let-out property

- Out of the multiple properties, any TWO (w.e.f 01/04/2019) property will be assumed to ‘self-occupied’, irrespective of the fact that the NRI is not residing in India. The income from such property will be assumed to be NIL.

- All other properties, other than mentioned in © above will be “let-out” or “Deemed to be let out” properties.

- It must be remembered that only property of which the possession is received can be taxed under the head — “Income from house property”. In other words, property under construction does not enter the ambit of taxation.

- In the case of “let-out” properties, the actual rent received is taxable.

- In the case of “deemed to be let-out” properties, a notional rent is presumed to be received and taxed accordingly (even if, none of the property is let-out in the real sense).

- There are specific and limited deduction given while calculating the taxable income under the head “Income from house property” as under:

- In the case of “let-out” and “deemed to be let-out” property there is no restriction on the amount of interest deduction. However, the total loss after aggregating all the income under the above 3 categories will be restricted to Rs.2,00,000/- in a year. This loss can be set off against other income. In other words, if the aggregate loss under the 3 categories is Rs.4.5 lakhs, then only Rs.2 lacs will be allowed as loss under the current year and the balance loss of Rs.2.5 lakhs will be carried forward to the subsequent 8 years for setting-off only against income from house property.

- Deduction on account of interest on loan cannot be claimed when the house is under construction. It can be claimed only after the construction is finished. The period from borrowing money until construction of the house is completed is called pre-construction period. Interest paid during this time can be claimed as a tax deduction in five equal installments starting from the year in which the construction of the property is completed.

- The interest deduction of Rs. 2,00,000/- in case of Self Occupied Property is subject to satisfaction of both the conditions as under

- The loan is taken on or after 1 April 1999

- The purchase or construction is completed within 5 years from the end of the FY in which loan was availed

- The interest deduction is restricted to Rs. 30,000 if the above conditions are not satisfied.

- Further, the total deduction for pre-construction period interest and the current period interest shall not exceed two lakh rupees.

- Suppose the NRI transfers the house property to the spouse for inadequate consideration and the spouse earns rental income on such property. The rental income will be taxed in the hands of the NRI and not the spouse because as per Section 27 of the Income Tax Act, the NRO will be the deemed owner of the property.

- Generally, the carried forward of loss is permissible provided the income tax return is filed by the due date. However, losses from house property is an exception to this rule and can be carried forward to future years even if return is not filed on time.

- Consider a situation wherein you have sold the property and subsequently, you receive some rent arrears/unrealized rent. Such income will continue to be taxed in the year of receipt under the head — “Income from house property” even though you are not the owner of that property. The only deduction available against such rent arrears/unrealized rent is the 30% standard deduction.

- l The 30% standard deductions and interest on loan deduction mentioned above is per person. Therefore, in the case of joint holding, each owner is entitled for such deduction.

- l Rental Income from sub-letting:

- Rental income in the hands of owner is charged to tax under the head “Income from house property”. Rental income of a person other than the owner cannot be charged to tax under the head “Income from house property”. Hence, rental income received by a tenant from sub-letting is taxable under the head “Income from other sources” or profits and gains from business or profession, as the case may be.

- income will be taxed in the hands of the NRI and not the spouse because as per Section 27 of the Income Tax Act, the NRO will be the deemed owner of the property.

- Generally, the carried forward of loss is permissible provided the income tax return is filed by the due date. However, losses from house property is an exception to this rule and can be carried forward to future years even if return is not filed on time.

- Consider a situation wherein you have sold the property and subsequently, you receive some rent arrears/unrealized rent. Such income will continue to be taxed in the year of receipt under the head — “Income from house property” even though you are not the owner of that property. The only deduction available against such rent arrears/unrealized rent is the 30% standard deduction.

- The 30% standard deductions and interest on loan deduction mentioned above is per person. Therefore, in the case of joint holding, each owner is entitled for such deduction.

Visit to know more about NRI Taxation Or www.gorantlaassociates.com

NRI Taxation Simplified:Understanding Residential Status and Taxes-Part 1

Understanding NRI Accounts and Taxation: Types and Implications — Part 2

Navigating NRI Capital Gains and Taxation: A Comprehensive Guide for Post-2018 Rules — Part — 3

Repatriating Property Sale Proceeds for NRIs: Process and Tax Implications — Part -4

Taxation Insights for Non-Resident Artistes, Entertainers, and Sportspersons in India — Part 5

NRI Tax Deductions and Special Provisions Under Chapter VI of the IT Act — Part 6

NRI and Foreign Citizen Taxation on Cross-Border Transactions — Part 7

Simplifying Taxation for NRIs with Blanket Deductions — Part 8

Disclaimer:

This Article/Blog has been contributed by Butchibabu Gorantla, B.Com, FCA, FCS, Chartered Accountant. This article/blog is posted with due authorization from the author for the academic purposes. The views and opinions expressed herein are those of the author and don’t constitute a legal advice to any user.

Related Posts

A Comprehensive Overview of the Finance Bill 2024

The Finance Bill 2024, introduced in the Lok Sabha, seeks to implement the financial proposals…

The Provisions of the Finance Bill, 2024: A Comprehensive Overview

The Finance Bill, 2024, introduces several amendments to the Income-tax Act, 1961, and other related…

Understanding the Income Tax Slab Rates for FY 2023-24, AY 2024-25: New vs. Old Tax Regimes

The income tax slab rate is the percentage of tax you pay on your income,…

Which ITR Form is Right for You? Find Out Now!

Filing your Income Tax Return (ITR) in India is an essential responsibility. However, with various…