SUMMARY OF PRESUMPTIVE PROVISIONS APPLICABLE TO NON-RESIDENTS

Example: Sea Port Shipping Line, a non-resident foreign company, is engaged in the business of carriage of goods shipped at Mumbai port. During the previous year ended on 31.3.2024, it had collected freight of ` 100 lakhs, demurrages of ` 20 lakhs and handling charges of ` 10 lakhs. The expenses of operating its fleet during the year for the Indian Ports were ` 110 lakhs. Compute its income applying the presumptive provisions under section 44B

Interpretation: Section 44B provides that in the case of an assessee, being a non-resident, engaged in the business of operation of ships, a sum equal to 7.5% of the aggregate of the following amounts would be deemed to be the profits and gains of such business chargeable to tax under the head “Profits and gains of business or profession”.

i) The amount paid or payable, whether within India or outside, to the assessee or to any person on his behalf on account of the carriage of passengers, livestock, mail or goods shipped at any port in India; and

ii) The amount received or deemed to be received in India by the assessee himself or by any other person on behalf of or on account of the carriage of passengers, livestock, mail or goods shipped at any port outside India.

The above amounts will include demurrage charges and handling charges

These provisions for computation of income from the shipping business in case of non-residents would apply notwithstanding anything to the contrary contained in the provisions of sections 28 to 43A of the Income-tax Act, 1961.

Therefore, in this case, M/s. Sea Port Shipping Line is required to pay tax in India on the basis of presumptive scheme as per the provisions of section 44B.

The assessee shall not be entitled to set off any of the expenses incurred for earning of such income. Therefore, the Shipping Line is required to pay tax on deemed profit of ` 9.75 lacs (7.50% on the total receipts of ` 130 lacs). The tax payable would be reduced by the amount of tax paid under section 172(4).

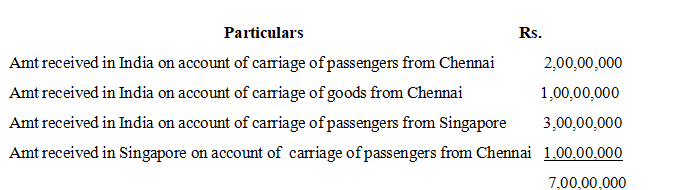

Example: Mr. Stephen, a non-resident, operates an aircraft between Singapore and Chennai. He received the following amounts while carrying on the business of operation of aircrafts for the year ended 31.3.2024:

(i) ` 2 crores in India on account of carriage of passengers from Chennai.

(ii) ` 1 crore in India on account of carriage of goods from Chennai.

(iii) ` 3 crores in India on account of carriage of passengers from Singapore.

(iv) ` 1 crore in Singapore on account of carriage of passengers from Chennai.

The total expenditure incurred by Mr. Stephen for the purposes of the business during the year ending 31.3.2024 was ` 6.75 crores.

Compute the income of Mr. Stephen chargeable to tax in India under the head “Profits and gains of business or profession” for the assessment year 2024–25.

What would be your answer in case the business was carried on by a foreign company, Stephen Airlines (P) Ltd?

Interpretation:

Section 44BBA says for computing profits and gains of the business of operation of aircraft in the case of non-residents a sum equal to 5% of the aggregate of the following amounts –

(a) paid or payable, whether in or out of India, to the assessee or to any person on his behalf on account of the carriage of passengers, livestock, mail or goods from any place in India; and

(b) received or deemed to be received in India by or on behalf of the assessee on account of the carriage of passengers, livestock, mail or goods from any place outside India.

Income from business under section 44BBA at 5% of ` 7,00,00,000 is ` 35,00,000, which is the income of Mr. Stephen chargeable to tax in India under the head “Profits and gains of business or profession” for the A.Y. 2024–25.

In case the assessee is a foreign company, say, Stephen Airlines (P) Ltd, the answer would be the same since section 44BBA does not distinguish corporate and non-corporate taxpayers who operate aircraft provided their residential status is that of non-resident.

Visit to know more about NRI Taxation Or www.gorantlaassociates.com

— –

Continue Read:

NRI Taxation Simplified:Understanding Residential Status and Taxes-Part 1

Understanding NRI Accounts and Taxation: Types and Implications — Part 2

Navigating NRI Capital Gains and Taxation: A Comprehensive Guide for Post-2018 Rules — Part — 3

Repatriating Property Sale Proceeds for NRIs: Process and Tax Implications — Part -4

Taxation Insights for Non-Resident Artistes, Entertainers, and Sportspersons in India — Part 5

NRI Tax Deductions and Special Provisions Under Chapter VI of the IT Act — Part 6

NRI and Foreign Citizen Taxation on Cross-Border Transactions — Part 7

Disclaimer:

This Article/Blog has been contributed by Butchibabu Gorantla, B.Com, FCA, FCS, Chartered Accountant. This article/blog is posted with due authorization from the author for the academic purposes. The views and opinions expressed herein are those of the author and don’t constitute a legal advice to any user.

Related Posts

July 25, 2024

A Comprehensive Overview of the Finance Bill 2024

The Finance Bill 2024, introduced in the Lok Sabha, seeks to implement the financial proposals…

July 25, 2024

The Provisions of the Finance Bill, 2024: A Comprehensive Overview

The Finance Bill, 2024, introduces several amendments to the Income-tax Act, 1961, and other related…

July 15, 2024

Understanding the Income Tax Slab Rates for FY 2023-24, AY 2024-25: New vs. Old Tax Regimes

The income tax slab rate is the percentage of tax you pay on your income,…

July 15, 2024

Which ITR Form is Right for You? Find Out Now!

Filing your Income Tax Return (ITR) in India is an essential responsibility. However, with various…