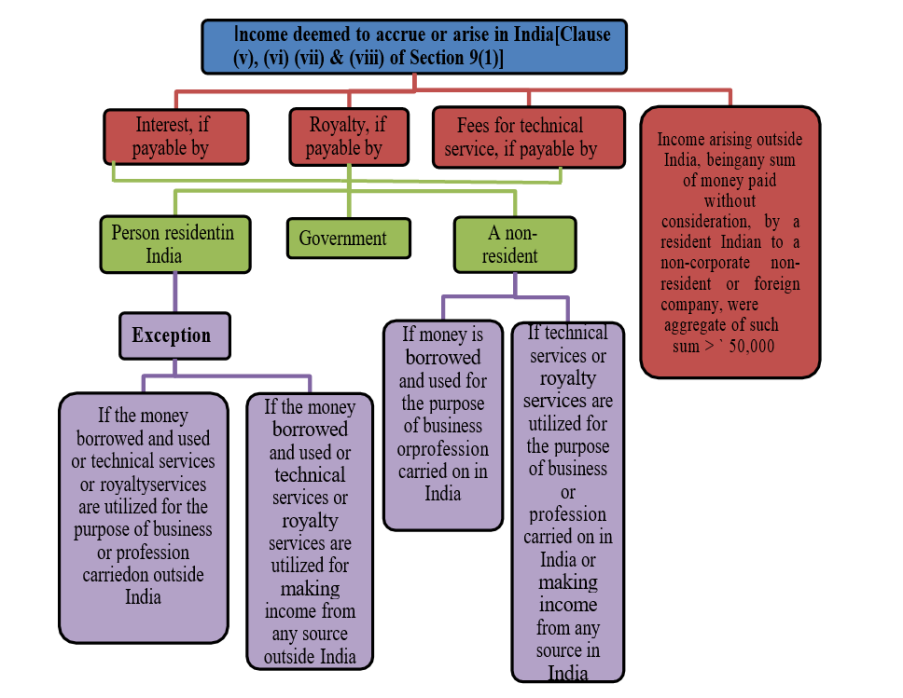

INCOME DEEMED TO ACCRUE OR ARISE IN INDIA TO A NON-RESIDENT BY WAY OF INTEREST, ROYALTY AND FEE FOR TECHNICAL SERVICES TO BE TAXED IRRESPECTIVE OF TERRITORIAL NEXUS [EXPLANATION TO SECTION 9]

Income by way of interest, royalty or fee for technical services which is deemed to accrue or arise in India, shall be included in the total income of the non-resident, whether or not –

i) the non-resident has a residence or place of business or business connection in India; or

ii) the non-resident has rendered services in India.

Fees for technical services (FTS) mean any consideration (including any lumpsum consideration) for the rendering of any managerial, technical or consultancy services (including providing the services of technical or other personnel). However, it does not include consideration for any construction, assembly, mining or like project undertaken by the recipient or consideration which would be income of the recipient chargeable under the head ‘Salaries’.

Example: Mr. Akhil, a citizen of India, left for USA for the purposes of employment on 1.5.2023. He has not visited India thereafter. Mr. Akhil borrows money from his friend Mr. Bharath, who also left India for employment purpose one week before Mr. Akhil’s departure, to the extent of ` 10 lakhs and buys shares in X Ltd., an Indian company. Discuss the taxability of the interest charged @10% in Bharath’s hands, if the said interest has been received in New York.

Interpretation: An individual is said to be resident in India in any previous year, if he –

i) has been in India during that year for a total period of 182 days or more, or

ii) has been in India during the four years immediately preceding that year for a total period of 365 days or more and has been in India for at least 60 days in that year.

In the case of an Indian citizen leaving India for the purposes of employment outside India during the previous year, the period of stay during the previous year in condition (ii) above, to qualify as a resident, would be 182 days instead of 60 days.

In this case, Mr. Akhil is an Indian citizen who left India for employment outside India on 01.05.2023. Mr. Akhil has been in India only from 1.4.2023 to 01.05.2023 i.e. for 31 days. Since his stay in India during the previous year 2023–24 is only 31 days, he does not satisfy the minimum criterion of 182 days stay in India for being a resident. Hence, his residential status for A.Y. 2024–25 is non-resident. Mr. Bharath, who left India one week before Akhil’s departure, is also a non-resident for the same reasons.

Section 9(1)(v) provides that income by way of interest payable by a non-resident in respect of any debt incurred, or moneys borrowed and used, for the purposes of a business or profession carried on by such person in India shall be deemed to accrue or arise in India.

Therefore, interest payable by a non-resident in respect of any debt incurred, or moneys borrowed and used, for the purpose of making or earning any income from any source other than a business or profession carried on by him in India, shall not be deemed to accrue or arise in India. Therefore, interest payable by Mr. Akhil on money borrowed from Mr. Bharath to invest in shares of an Indian company shall not be deemed to accrue or arise in India and hence, is not taxable in India in the hands of Mr. Bharath.

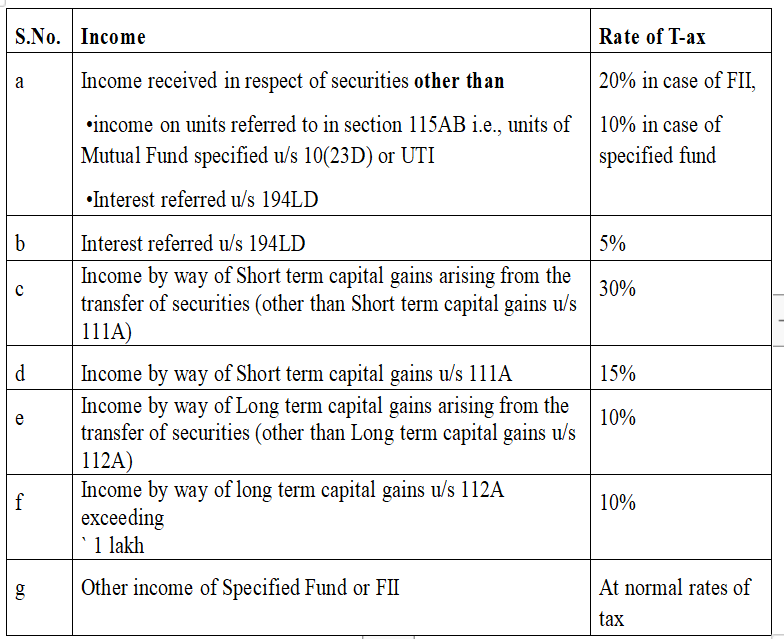

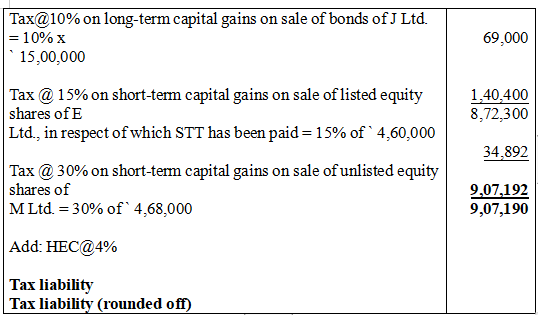

Special provisions for computing tax on income of Specified Fund or Foreign Institutional Investors from securities or capital gains arising from their transfer [Section 115AD]

Example: Eagle Inc., a notified Foreign Institutional Investor (FII), derived the following incomes for the financial year 2023–24: –

(1) Interest received on investment in Rupee Denominated Bonds of ABC Ltd., an Indian company (investment was made in the F.Y.2022–23) — ` 8,50,000

(2) Dividend from listed shares of Indian companies — ` 6,20,000

(3) Interest on securities — ` 17,32,000 (Expenses of ` 26,000 has been incurred to earn such income)

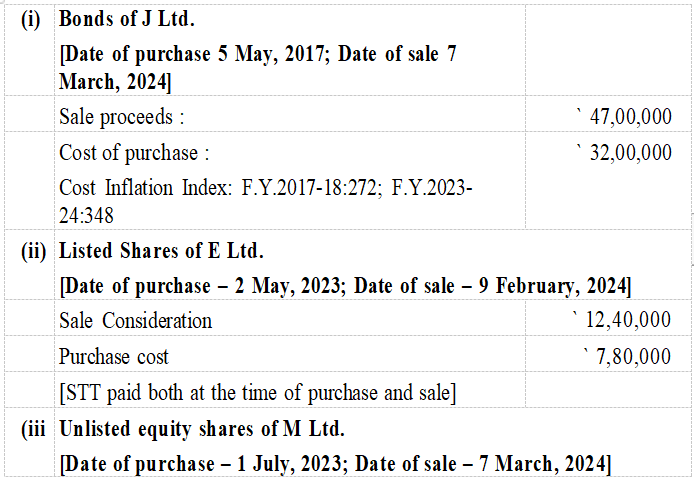

(4) Income from sale of securities and shares:

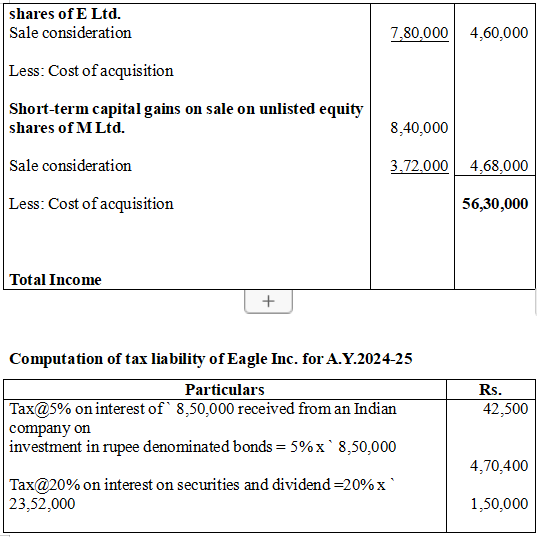

Compute the total income and tax liability of the FII, STYLE Inc., for the A.Y. 2024–25 as per section 115AD, assuming that no other income is derived by STYLE Inc. during the F.Y.2023–24.

Interpretation:

Total income of Eagle Inc., a notified FII, for A.Y.2024–25

— –

Continue Read:

NRI Taxation Simplified:Understanding Residential Status and Taxes-Part 1

Understanding NRI Accounts and Taxation: Types and Implications — Part 2

Navigating NRI Capital Gains and Taxation: A Comprehensive Guide for Post-2018 Rules — Part — 3

Repatriating Property Sale Proceeds for NRIs: Process and Tax Implications — Part -4

Taxation Insights for Non-Resident Artistes, Entertainers, and Sportspersons in India — Part 5

NRI Tax Deductions and Special Provisions Under Chapter VI of the IT Act — Part 6

Disclaimer:

This Article/Blog has been contributed by Butchibabu Gorantla, B.Com, FCA, FCS, Chartered Accountant. This article/blog is posted with due authorization from the author for the academic purposes. The views and opinions expressed herein are those of the author and don’t constitute a legal advice to any user.

Related Posts

July 25, 2024

A Comprehensive Overview of the Finance Bill 2024

The Finance Bill 2024, introduced in the Lok Sabha, seeks to implement the financial proposals…

July 25, 2024

The Provisions of the Finance Bill, 2024: A Comprehensive Overview

The Finance Bill, 2024, introduces several amendments to the Income-tax Act, 1961, and other related…

July 15, 2024

Understanding the Income Tax Slab Rates for FY 2023-24, AY 2024-25: New vs. Old Tax Regimes

The income tax slab rate is the percentage of tax you pay on your income,…

July 15, 2024

Which ITR Form is Right for You? Find Out Now!

Filing your Income Tax Return (ITR) in India is an essential responsibility. However, with various…